Financial Statements And Related Announcement - Full Yearly Results

Financials Archive![]() Note: Files are in Adobe (PDF) format.

Note: Files are in Adobe (PDF) format.

Please download the free Adobe Acrobat Reader to view these documents.

Condensed interim consolidated statement of profit or loss and other comprehensive income

Condensed interim statements of financial position

Review Of Performance

COMPARING 3 MONTHS ENDED 31 DECEMBER 2025 ("Q4FY2025") AGAINST 3 MONTHS ENDED 31 DECEMBER 2024 ("Q4FY2024")

Income Statement

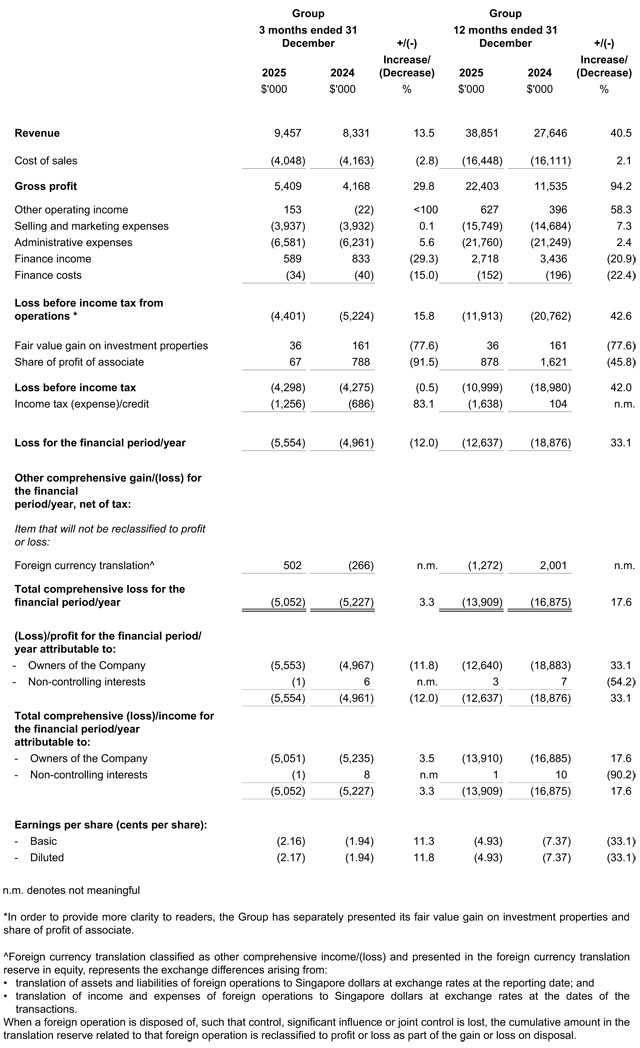

Revenue

Revenue increased by 13.5% year-over-year ("yoy") from S$8.3 million in Q4FY2024 to S$9.5 million in Q4FY2025, mainly due to a one-off revenue reversal of approximately S$0.9 million recorded in Q4FY2024 in relation to Refund/Waiver for High Risk Tanks, which lowered the banking revenue in the prior year. Banking revenue increased by 14.5% yoy from S$7.5 million in Q4FY2024 to S$8.5 million in Q4FY2025.

Diagnostic revenue increased by 5.3% yoy, or S$47 thousand, to S$0.9 million in Q4FY2025, mainly attributable to higher testing volume in Hong Kong and Philippines, partially offset by lower contributions from certain other markets.

Gross profit and gross profit margin

Gross profit increased from S$4.2 million in Q4FY2024 to S$5.4 million in Q4FY2025 mainly due to higher revenue during the quarter and the absence of the one-off Refund/Waiver for High-Risk Tanks of approximately S$0.9 million recorded in Q4FY2024, which had reduced the prior year's gross profit.

The gross profit margin improved to 57.2% in Q4FY2025 from 50.0% in Q4FY2024, supported by the normalisation of gross margins following the one-off impact in the prior year.

Other operating income

Other operating income increased by approximately S$0.2 million yoy in Q4FY2025 compared to Q4FY2024 was mainly due to the increase in talent funding received in Hong Kong.

Administrative expenses

Administrative expenses increased by 5.6% or S$0.4 million in Q4FY2025 compared to Q4FY2024, mainly attributable to higher loss on disposal of fixed assets of approximately S$0.2 million, increased rental expenses of about $0.1 million, and higher staff costs of approximately $0.1 million.

Finance income

Finance income decreased by S$0.2 million from Q4FY2024 to Q4FY2025 mainly due to the lower average deposit rate for Q4FY2025 as compared to Q4FY2024 and a decrease in funds placed in fixed deposits.

Finance costs

Finance costs relate to lease liabilities amounted to S$34,000 (Q4FY2024: S$40,000). The decrease was mainly due to decrease in lease liabilities recognised in Q4FY2025 as compared to Q4FY2024.

Loss before income tax from operations

As a result of the foregoing, the Group recorded a loss before income tax from operations of S$4.4 million in Q4FY2025, compared with a loss before income tax from operations of S$5.2 million in Q4FY2024.

Share of profit of associate

In Q4FY2025, the Group recognised the share of profit of associate of S$0.1 million, lower than the S$0.8 million recognised in Q4FY2024.

Tax

Over-provision of tax in respect of prior years of S$54,000 for Q4FY2025 mainly comprises overprovision of deferred tax liability for prior years of S$35,000 in Indonesia, S$14,000 in Singapore and S$6,000 in Malaysia, offset by an under-provision of S$1,000 by Philippines.

In Q4FY2024, the under-provision of tax in respect of prior years of S$159,000 mainly comprises under-provision of corporate tax of S$212,000 in Singapore, S$166,000 in Philippines and S$13,000 in Indonesia respectively, offset by an over-provision of corporate tax in Singapore of S$232,000.

Adjusting for the foregoing, the Group recorded lower tax expenses in Q4FY2025 mainly due to lower tax assessment in Indonesia, Malaysia, Hong Kong and Philippines.

COMPARING 12 MONTHS ENDED 31 DECEMBER 2025 ("FY2025") AGAINST 12 MONTHS ENDED 31 DECEMBER 2024 ("FY2024")

Income Statement

Revenue

Revenue increased by 40.5% or S$11.2 million from S$27.6 million in FY2024 to S$38.9 million in FY2025. The increase was mainly driven by higher banking revenue, which rose by approximately 45.7% or S$10.8 million, from S$23.7 million in FY2024 to S$34.6 million in FY2025.

FY2024 revenue included a one-off revenue reversal of approximately S$10.6 million, which lowered the prior year comparative base. Excluding this reversal, FY2025 revenue of S$38.9 million would represent an increase of approximately 1.8% year-on-year ("yoy") compared with an adjusted FY2024 revenue base of about S$38.2 million.

On a geographical basis, the yoy revenue movement was mainly driven by Singapore, Hong Kong and Malaysia. Singapore resumed its full operation during the period 14 January 2025 and 29 September 2025. Hong Kong remained one of the largest contributors to Banking revenue and was broadly stable yoy, while Malaysia recorded a notable increase in Banking revenue compared to FY2024. These improvements were partially offset by lower contributions from certain other markets.

Diagnostics revenue increased by 9.2% or S$0.4 million from FY2024 to FY2025, mainly driven by higher testing revenue in Hong Kong and the Philippines, with additional contribution from Indonesia, partially offset by lower testing volumes in Singapore, Malaysia and India.

Gross profit and gross profit margin

Gross profit increased from S$11.5 million in FY2024 to S$22.4 million in FY2025,mainly due to the absence of financial impact of Refund/Waiver for High-Risks Tanks of S$10.6 million recognised in FY2024 and improved operating contribution across selected markets.

Excluding the financial impact of the refunds of approximately S$10.6 million recognised in FY2024, gross profit in FY2024 would have been approximately S$22.1 million. On this normalised basis, FY2025 gross profit of S$22.4 million represents a 1.4% yoy increase.

Gross profit margin improved from 41.7% in FY2024 to 57.7% in FY2025. The margin improvement primarily reflects the impact of the FY2024 refund adjustments, which had reduced prior year gross profit and margin, together with more stable cost absorption and service mix in FY2025.

Other operating income

Other operating income increased by approximately S$0.2 million in FY2025 compared to FY2024. The increase was mainly due to talent funding received in Hong Kong.

Selling and marketing expenses

Selling and marketing expenses increased by 7.3% or S$1.1 million in FY2025 compared to FY2024, primarily driven by higher selling and marketing activities in Singapore, as FY2024 included a suspension period whereas FY2025 reflected a higher level of commercial engagement.

Administrative expenses

Administrative expenses for FY2025 of S$21.8 million increased by 2.4% or S$0.5 million compared to FY2024 of S$21.2 million. This is mainly due to an increase of approximately S$0.4 million in impairment loss on trade receivables, S$0.2 million in loss on disposal, S$0.4 million in director fees and staff costs and S$0.2 million in insurance expenses. This is partially offset by S$0.7 million decrease in legal & consultancy fees.

Finance income

Finance income comprises interest income from deposits, short-term investments and note receivable of S$2.7 million and decreased comparable to that of FY2024. Mainly due to the lower average deposit rate and a decrease in funds placed in fixed deposits.

Finance costs

Finance costs relate to lease liabilities which amounted to S$0.2 million (FY2024: S$0.2 million). The decrease was largely due to a decrease in lease liabilities recognised in FY2025 as compared to FY2024.

Loss before income tax from operations

As a result of the foregoing, the Group incurred a loss before income tax from operations of S$11.9 million for FY2025 as compared to a loss before income tax of S$20.8 million for FY2024.

Fair value gain on investment properties

In FY2025, the Group recognised fair value gain of S$36,000 (FY2024: S$0.2 million) on its investment properties held in Singapore and Malaysia.

Share of profit of associate

In FY2025, the Group recognised the share of profit of associate of S$0.9 million, which was a (45.8)% decrease compared to S$1.6 million recognised in FY2024.

Tax

In both FY2025 and FY2024, fair value gain on investment properties was not taxable.

Under-provision of tax in respect of prior years of approximately S$83,000 for FY2025 mainly comprises under-provision of corporate income tax of S$138,000 in Philippines, offset by an overprovision of deferred tax liability for prior years of S$35,000 in Indonesia and over- provision of corporate income tax of S$6,000 and S$14,000 in Malaysia and Singapore respectively.

In FY2024, the under-provision of tax in respect of prior years of S$159,000 mainly comprises under-provision of corporate tax of S$212,000 in Singapore, S$166,000 in Philippines and S$13,000 in Indonesia respectively , offset by an over-provision of corporate tax in Singapore of S$232,000.

Adjusted for the foregoing, the Group recorded a higher tax expense for FY2025 compared to the tax expenses in FY2024.

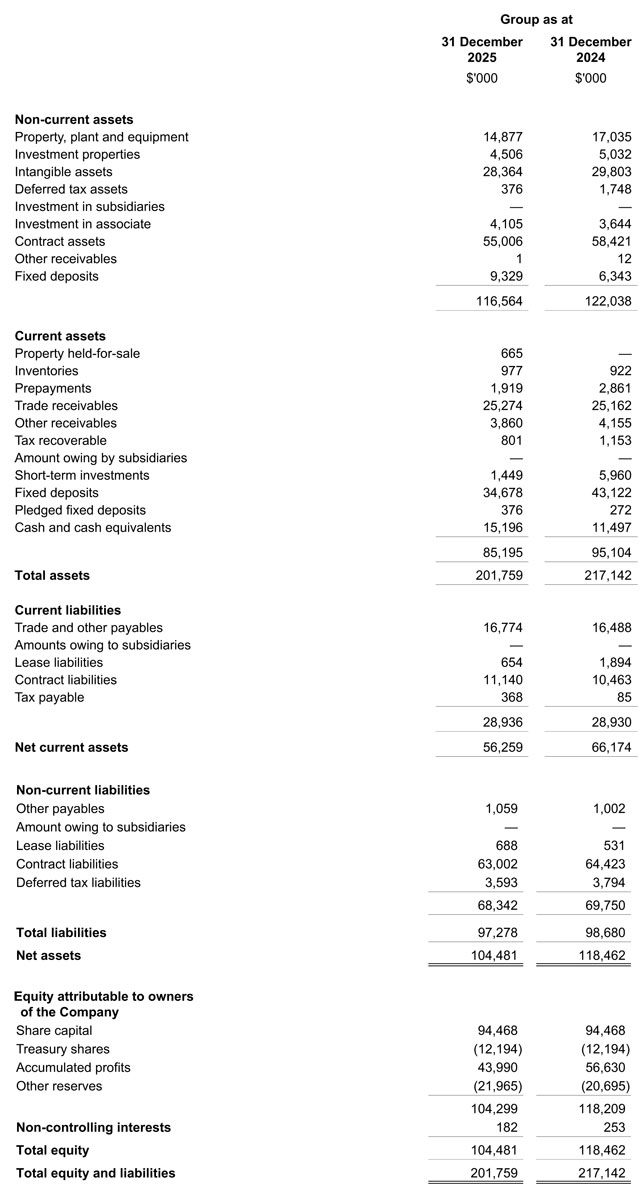

Balance sheet

Cash and cash equivalents, unpledged and pledged fixed deposits ("fixed deposits"), short-term investments ("investments")

As at 31 December 2025, the Group maintained a strong balance sheet, with cash and cash equivalents, fixed deposits, investments of S$61.0 million (31 December 2024: S$67.2 million). Investments mainly comprise of short-term investments in money market funds.

The increase in cash and cash equivalents of S$3.7 million from S$11.5 million as at 31 December 2024 to S$15.2 million as at 31 December 2025 was mainly due to cash from operating activities of S$44,000, redemption of short-term investments of S$4.2 million, transfer from short-term fixed deposit of S$3.3 million, offset by the purchase of property, plant and equipment and intangible assets of S$1.5 million and payment of lease liabilities of S$2.0 million.

Net cash used in operating activities comprised mainly operating cash flows before movements in working capital of S$7.8 million, net working capital inflow of S$5.1 million and net interest received of S$2.6 million offset by net income taxes paid of S$0.1 million.

Net working capital inflow of approximately S$5.1 million comprised the following:

- increase in trade receivables of approximately S$2.5 million;

- decrease in contract assets of approximately S$2.2 million;

- decrease in other receivables, deposits and prepayments of approximately S$1.5 million;

- increase in inventories of approximately S$55,000;

- increase in trade and other payables of approximately S$0.9 million;

- increase in contract liabilities of approximately S$3.1 million.

The decrease in current and non-current fixed deposits and short-term investments of S$9.9 million is mainly due to the redemption of the Class A Redeemable Convertible Note ("RCN") amounting to S$4.2 million, a net transfer of S$3.3 million from term deposits to cash and cash equivalents, as well as a translation loss of S$2.0 million on fixed deposits in the subsidiaries in Malaysia and India due to weakening of the Malaysian Ringgit and Indian Rupee against the Singapore Dollar.

Property, plant and equipment

As at 31 December 2025, the Group recorded S$14.9 million on its balance sheet for property, plant and equipment (31 December 2024: S$17.0 million). The decrease in property, plant and equipment is due to depreciation of approximately S$3.7 million and exchange differences of S$0.6 million, offset by addition of S$2.3 million in FY2025.

Investment properties

As at 31 December 2025, the Group recorded S$4.5 million on its balance sheet for investment properties (31 December 2024: S$5.0 million). The decrease is mainly due to the transfer of certain Malaysian properties to property held for sales.

Intangible assets

Intangible assets comprise client contracts, brand and goodwill acquired in business combinations and computer software.

Deferred tax assets

As at 31 December 2025, the Group recorded deferred tax assets of S$0.4 million. (31 December 2024 : S$1.7 million). The deferred tax assets represent prior year tax losses carried forward as a result of the transitional adjustments arising from the adoption of FRS115 in the Hong Kong subsidiary and unutilised merger and acquisition allowance, relating to acquisitions made by the Company in previous years. The decrease during the year is mainly due to the reversal of deferred tax assets previously recognised in Singapore.

Investment in associate

Investment in associate comprises a 39.61% stake in TSL through Stemlife Berhad. The increase in investment in associate was due to the recognition of the share of profit of associate of S$0.9 million in FY2025, slightly offset by the dividend received from TSL.

Contract assets, non-current

Non-current contract assets represent all service revenues arising from the performance obligations identified under installment payment plans in the cord blood, cord lining and cord tissue banking contracts that have yet to be billed to clients. Upon billing, the billed amount will be receivable under the same terms as the current trade receivables. As at 31 December 2025, the Group recorded non-current contract assets of S$55.0 million (31 December 2024: S$58.4 million).

Property held for sales

As at 31 December 2025, the Group recorded S$0.7 million (31 December 2024: Nil) as property held-for-sales. This reflects the Group's strategic decision to divest specific interests in Malaysia.

Inventories

As at 31 December 2025, the Group recorded inventories of S$1.0 million (31 December 2024: S$0.9 million).

Prepayments

As at 31 December 2025, the Group recorded prepayments of S$1.9 million (31 December 2024: S$2.9 million). The decrease is mainly due to Singapore where there is prior year prepayment was utilised during the year and a decrease in prepaid booking fees for future participation in baby fair.

Trade receivables, current

Current trade receivables as at 31 December 2025 was S$25.3 million compared to S$25.2 million as at 31 December 2024.

Other receivables

As at 31 December 2025, the Group recorded other receivables of S$3.9 million (31 December 2024: S$4.2 million). The decrease is mainly due to decrease in deposits placed and return of existing deposits.

Short-term investments

As at 31 December 2025, the Group recorded short-term investments of S$1.4 million (31 December 2024: S$6.0 million). The decrease was mainly due to redemption of a RCN in the principal amount of S$4.2 million on 31 December 2024, which was subsequently received during the year, The amount as at 31 December 2025 mainly comprises money market funds held in Malaysia.

Trade and other payables, current and non-current

As at 31 December 2025, the Group recorded current trade and other payables of S$16.8 million (31 December 2024: S$16.5 million) and non-current other payables of S$1.1 million (31 December 2024: S$1.0 million). This was mainly due to the provision for warranty expense of S$0.3 million recognised as part of the Enhanced Package offered to the affected customers in Singapore.

Lease liabilities, current and non-current

As of 31 December 2025, the Group recognised lease liabilities of S$1.3 million on property and equipment leases (31 December 2024: S$2.4 million). The decrease in lease liabilities was attributable to the payments made during the year.

Contract liabilities, current and non-current

Contract liabilities represent revenue received in advance for services revenues to be rendered under the various performance obligations identified in the cord blood, cord lining, cord tissue banking and diagnostics contracts. As at 31 December 2025, current and non-current contract liabilities were at S$11.1 million and S$63.0 million respectively (31 December 2024: S$10.5 million and S$64.4 million respectively).

Income tax payable

The Group's income tax payable increased by S$0.3 million from 31 December 2024 due to tax in Philippines and Indonesia.

Deferred tax liabilities

As at 31 December 2025, deferred tax liabilities amounted to S$3.6 million (31 December 2024: S$3.8 million), comprising deferred tax liabilities on temporary differences and on intangible assets recognised on business combination.

Commentary

As announced by the Company on 1 March 2025, 1 April 2025 and 14 August 2025, there were claims made by or on behalf of persons who have identified themselves as clients of the Company. As elaborated in Note 2(a), on 1 December 2025, OA 1365 was filed against the Company by the Representative.

The Company has been seeking legal advice, and in consultation with its legal advisers, actively monitoring and attending to the claims and will take necessary steps to engage with the relevant parties at the appropriate juncture.

The exposure from the claims remains uncertain and the Company is unable to determine the impact of the Claims on the Group's financial performance and prospects for the financial year ending 31 December 2026 ("FY2026"). However, should the Company be ultimately required to settle all the Claims made by multiple clients in FY2026, this will likely result in a negative impact on the financial position of the Group for FY2026.

As announced by the Company on 13 October 2025, since 30 September 2025, the Company has stopped the collection, testing, processing and/or storage of any new cord blood units in Singapore.

The Company's CBBS Licence has been modified through the addition of the licence conditions as elaborated in Note 2(a). For the avoidance of doubt, these licensing conditions only relate to the Company's operations in Singapore. The Group's business activities in all other jurisdictions (namely, Malaysia, Hong Kong, India, Philippines, Indonesia, and Thailand) are in full operation and the licences maintained by those respective countries under the Group in those jurisdictions remain in full force and effect.

Due to the uncertainties faced by the Company in view of the licensing conditions, the investigations in relation to the Remaining 3 Tanks as well as the status of the Company's operations in Singapore, the Company is unable to assess the financial impact on the Group's financial performance and prospects for FY2026.

However, should the Company be unable to meet all the requirements of the CBBS Licence in the Singapore operation, this will likely result in a negative impact on the financial position of the Group for FY2026. Please refer to Note 2(a) for the additional conditions to the Company's CBBS Licence.

The Group maintains optimism for its cord blood banking and diagnostics business, driven by rising demand for stem cell-based therapies, amid growing prevalence of chronic genetic, neurological and blood disorders. Parents are increasingly opting to bank cord blood for future therapeutic use, encouraged by government initiatives and favourable policies, according to Credence Research, a leading international provider of market intelligence on the industry.

Most market analysts are projecting Southeast Asia's umbilical cord blood market to grow by double-digit compounded annual growth rate in the next five years, with the storage segment continuing to dominate. Barriers to market entry are significant due to the high cost of cord blood banking and the strict regulatory regime around the commercialisation of human tissue.

Outside Singapore, the Group intends to strengthen its quality control over the cord blood, cord lining and tissue banking services while deepening partnerships with doctors and hospitals in the region. It also plans to enhance awareness of stem cell applications in clinical practice.